By HASE Fiero | IE Press — Information Warfare

There is no conspiracy here. There doesn’t need to be. The system works exactly as designed, and the design is profitable.

The Pitch

Somewhere in Boca Raton, a quarterly earnings call is underway. The CEO is upbeat. Occupancy rates are climbing. Four dormant facilities have been reactivated. Revenue guidance is raised. The product being sold is not software, not logistics, not even real estate.

The product is a human body in a bed, billed to the federal government at $164.65 per day.

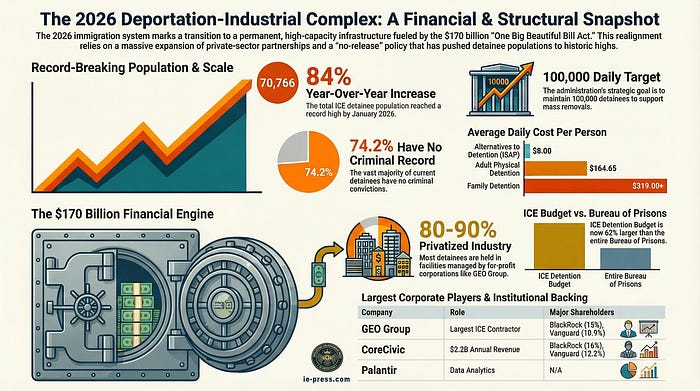

This is not an opinion piece about whether mass detention is right or wrong. This is a systems analysis of how the largest expansion of immigration incarceration in American history has been engineered — legislatively, financially, and operationally — to function as a permanent, investable market. If you want to understand who profits from the detention of 70,766 people and counting, you need to follow the architecture, not the rhetoric.

Step One: Secure the Funding — The “One Big Beautiful Bill Act”

Every industrial complex needs a budget line. The military-industrial complex has the National Defense Authorization Act. The deportation-industrial complex now has the “One Big Beautiful Bill Act” (H.R. 1), signed into law in July 2025.

The numbers are not subtle. The OBBBA allocates $170 billion over four years for border and interior enforcement. Of that, roughly $75 billion flows directly to ICE, giving the agency access to approximately $29 billion in a single fiscal year — triple its entire FY 2024 budget. The detention-specific carve-out is $45 billion, earmarked for building new centers, reactivating shuttered ones, and maintaining infrastructure for 100,000 to 135,000 beds.

To put this in proportion: ICE’s annual detention budget now exceeds the entire budget of the Federal Bureau of Prisons by 62%. The Bureau of Prisons houses 155,000 inmates. ICE’s target is 100,000 — and it hasn’t gotten there yet.

This is not a one-year surge. The four-year funding rollover ensures that the infrastructure outlasts any single political cycle. Even if enforcement priorities shift in 2029, the facilities will already be built, the contracts will already be signed, and the corporations will already be reporting the revenue.

The playbook’s first rule: make the money structural, not discretionary.

Step Two: Build the Capacity — 212 Facilities and Counting

As of December 2025, ICE operates 212 active detention centers — nearly double the network from twelve months earlier. The expansion follows a geographic logic anchored to the southern border and Gulf Coast, but it is increasingly national. Facilities in the Northeast and Midwest are being reactivated. Military bases like Fort Bliss are being repurposed. A site in the Florida Everglades — colloquially “Alligator Alcatraz” — has been authorized.

The facility types reveal the strategy’s modularity:

Service Processing Centers (SPCs) are ICE-owned and operated — the agency’s home turf. Contract Detention Facilities (CDFs) are owned and run entirely by private corporations. Inter-Governmental Service Agreements (IGSAs) route federal detainees into county jails, where the locality receives a per-diem cut while a private operator manages the day-to-day. Short-term staging warehouses in Virginia, Texas, Louisiana, Arizona, Georgia, and Mississippi serve as final processing hubs before removal flights.

The largest single facility — Ero El Paso Camp East Montana — holds nearly 3,000 people per day. Adams County Correctional Center in Natchez, Mississippi, holds 2,162. Stewart County in Lumpkin, Georgia: 2,011. These are not temporary holding cells. They are small cities.

The speed of expansion has outrun oversight. The Krome North facility in Florida was documented at 295% capacity — 1,800 people in a space designed for 611. Private operators routinely obtain waivers exempting them from federal detention standards. Meanwhile, facility inspections by the Office of Detention Oversight dropped 36% in 2025.

The playbook’s second rule: build faster than anyone can inspect.

Step Three: Fill the Beds — The 74.2% Problem

The operational logic of mass detention requires volume. Volume requires bodies. And the bodies, as it turns out, don’t need to be criminals.

As of January 2026, 74.2% of all ICE detainees — 52,504 out of 70,766 — have no criminal record. Among those who do, many were convicted of traffic violations. The population of non-criminal detainees arrested in “at-large” interior operations grew by 2,500% in twelve months. Discretionary releases on bond fell by 87% under the administration’s “no release” directive.

In December 2025 alone, 42,128 individuals were booked into the system. Of those, 37,842 were arrested by ICE officers in the interior — not at the border. This is not border enforcement. This is community-level dragnet policing optimized for throughput.

Approximately 6,000 individuals are held in family staging centers, including parents and minors. The Dilley facility in Texas — operated by CoreCivic — has been reactivated specifically for this purpose. Family detention was previously phased out. It has been quietly restored.

The playbook’s third rule: the beds don’t fill themselves — redefine who belongs in them.

Step Four: Privatize the Operation — The Duopoly

Between 80% and 90% of all immigration detainees are held in facilities owned or managed by two companies: The GEO Group and CoreCivic. Both have described the 2025–2026 period as a “pivotal moment” and a “gold rush.”

The GEO Group

Headquartered in Boca Raton, Florida. ICE’s largest contractor. In 2025, GEO invested nearly $100 million to expand its detention, transportation, and electronic monitoring capabilities. The company reactivated four major facilities with 6,600 beds for ICE, projected to generate over $240 million in annual revenue.

Key moves: The Adelanto ICE Processing Center in California reopened after a COVID-era ban was lifted — 1,940 beds. Delaney Hall in New Jersey opened under an ICE contract valued at $1 billion over its term. North Lake in Michigan added 1,800 beds, expected to produce $85 million annually at full occupancy.

GEO’s subsidiary, GTI, is the largest provider of ground and air transportation for ICE removals, projecting an additional $40–50 million in annual revenue from deportation flights. Another subsidiary, BI Incorporated, monitors 182,000 people through the Intensive Supervision Appearance Program — the “digital prison” that feeds the physical one.

CoreCivic

Based in Brentwood, Tennessee. Total revenue exceeded $2.2 billion in 2025 — a 13% year-over-year increase driven by new ICE contracts. The company reactivated four of nine previously idle facilities. The Dilley Immigration Processing Center in Texas (2,400 beds, $180 million in annual revenue) now houses families. The California City facility (2,560 beds, $130 million annually) moved to a long-term contract. A repurposed federal prison in Leavenworth, Kansas, added over 1,000 beds.

CoreCivic’s ICE management revenue more than doubled in Q4 2025 compared to the prior year.

The playbook’s fourth rule: the government builds the mandate; the corporation builds the margin.

Step Five: Lock in the Revolving Door

The boundary between the agency and its contractors is not a wall. It’s a turnstile.

Daniel A. Bible — the ICE career official who oversaw Enforcement and Removal Operations — left the agency on October 31, 2024, and became an Executive Vice President at GEO Group just as mass deportation plans were finalized. Daniel Ragsdale, former ICE Deputy Director, joined GEO as an executive in 2017. Julie M. Wood, former ICE Director under the Bush administration, joined GEO’s board in 2014. David Venturella, former head of ICE detention and removal, became a GEO executive in 2012.

These are not coincidences. They are structural features. Former officials bring institutional knowledge of procurement cycles, agency budgets, and contract architecture. They don’t just work for the companies — they are the bridge between public mandate and private execution.

The financial dimension is equally direct. For the 2024 cycle and inaugural efforts, CoreCivic and GEO Group, along with their PACs and executives, donated nearly $2.8 million to the current administration. GEO’s PAC alone distributed over $4 million to federal and state candidates.

The playbook’s fifth rule: hire the people who write the contracts, then write the next contract.

Step Six: Financialize the Whole Thing

Private detention is not a cottage industry. It is a publicly traded, institutionally owned, Wall Street–integrated asset class.

BlackRock holds 15.05% of GEO Group and 16.03% of CoreCivic. Vanguard holds 10.89% and 12.16%, respectively. State Street holds 3.75% of CoreCivic. These are not activist investors. They are index fund managers — which means the retirement savings of millions of ordinary Americans are passively invested in the operational capacity to detain 70,766 people.

The stock performance has been volatile. Following the 2024 election, GEO Group’s share price nearly tripled, reaching $36.46. By January 2026, it had corrected to around $16, as the logistical reality of hiring 10,000 officers and reactivating dozens of sites proved slower than Wall Street’s expectations. But the underlying revenue fundamentals remained strong — CoreCivic’s ICE revenue more than doubled in Q4.

The market’s message is clear: the thesis isn’t whether detention will expand. It’s how fast.

The playbook’s sixth rule: turn human confinement into a line item on a pension fund’s balance sheet.

The Cost Structure — What a Body in a Bed Actually Costs

The per-diem economics are the engine:

Custody Type Daily Cost Per Person Alternatives to Detention (ISAP) $8.00 Community Case Management $14.05 Local Jail Detainer $71.44 Adult Physical Detention $164.65 Family Detention $319.00+ Specialized Medical/Subacute $771–$1,553

At the target population of 100,000, adult detention alone runs $16.4 to $18.7 million per day — roughly $6 to $6.8 billion annually — before transportation, legal costs, or facility construction. The full-cycle cost of a single deportation, from arrest through months of detention to chartered removal flight, is estimated to reach or exceed $1.5 million per person.

Alternatives to Detention cost a fraction of physical incarceration. ISAP runs $8 per day. Community case management: $14. But the policy framework explicitly favors beds over bracelets. The number of individuals in ATD has decreased as funding flows toward physical custody.

This is not an efficiency calculation. It’s a volume calculation. Every empty bed is lost revenue. Every body in that bed is a billable day. The incentive structure does not optimize for cost — it optimizes for capacity utilization.

The Opportunity Cost — What $170 Billion Doesn’t Buy

The $170 billion authorized by the OBBBA was passed alongside significant cuts to social services. Between 12 and 17 million Americans are at risk of losing healthcare or nutritional assistance as federal spending realigns toward the deportation apparatus. The immigration enforcement budget now eclipses the combined budgets of all other non-immigration federal law enforcement agencies.

This is the part that never makes it into the earnings call. The money that funds 100,000 beds is money that doesn’t fund clinics, schools, food assistance, or housing. The fiscal architecture of mass detention is not an addition to the federal budget — it’s a substitution within it.

The Uncomfortable Arithmetic

Here is what the playbook produces when you run the numbers to their conclusion:

70,766 people currently detained, 74.2% with no criminal record

212 active facilities, nearly doubled in twelve months

$29 billion in annual ICE funding, triple the prior year

$45 billion earmarked for detention infrastructure through 2029

80–90% of detainees held in for-profit facilities

$2.8 million in political contributions from the duopoly to the current administration

2,500% increase in non-criminal interior arrests

87% decrease in discretionary bond releases

36% decrease in facility oversight inspections

12–17 million Americans at risk of losing social services to fund the expansion

This is not a system that accidentally became profitable. Profitability is the load-bearing structure. Remove the profit motive and the political contributions dry up, the revolving door stops spinning, the facilities don’t get built, and the beds don’t get filled.

The question was never “how do you profit from mass detention?”

The question is: can the system function without the profit?

A Note on “Investing the Theme”

For those approaching this as a financial question — and many will — the due diligence framework is straightforward:

Confirm revenue linkage. Do the filings name DHS/ICE as a major customer? What percentage of revenue comes from government contracts?

Inspect contract durability. Multi-year facility contracts are harder to unwind than short-term service agreements. Look at backlog, remaining performance obligations, and renewal commentary.

Stress test the political scenario. What happens after an election? What if courts block practices? What if state restrictions tighten?

Quantify the friction. Litigation, settlements, compliance upgrades, financing risk, and reputation-driven investor pressure are real costs — and they’re nonlinear.

Decide your ethical boundary in writing. Before you invest. Not after.

The market doesn’t always reward the obvious — especially when society decides the obvious shouldn’t exist.

Closing

There is a word for a system in which the government creates demand, private corporations supply capacity, former officials broker the relationship, Wall Street finances the operation, and the product is the physical confinement of human beings — most of whom have committed no crime.

The word is industry.

And like every industry, it has a playbook. Now you’ve read it.

HASE Fiero is the author of The Dark Enlightenment Series and the founder of Intellectual Enlightenment Press, llc. This article is published under the IE Press — Information Warfare imprint.

Sources: DHS internal data, ICE booking statistics (FY 2025–2026), Congressional Budget Office analysis of H.R. 1, SEC filings (GEO Group 10-K, CoreCivic 10-K), OpenSecrets political contribution data, American Immigration Council fiscal analysis, Office of Detention Oversight inspection reports.